Trump's Trade War Gambit: Why America May Lose More Than China in Tariff Escalation

Author: Luis Flavio | October 10, 2025 03:28pm

In a fiery Truth Social post Friday morning, President Donald Trump threatened China with a “massive increase of Tariffs” on imports, potentially canceling his planned meeting with Xi Jinping after Beijing unveiled sweeping rare-earth export controls. Markets immediately reacted, with the S&P 500 dropping 1.56% and the Nasdaq falling 2.05% as Wall Street absorbed the escalation.

Trump’s response to China’s rare-earth crackdown sets up the most significant trade confrontation since early 2025. But here’s the uncomfortable truth emerging from economic models: America may suffer deeper economic damage than China from the very tariffs Trump is threatening to impose.

The data tells a counterintuitive story. Research shows American consumers could face an additional 2-4% inflation surge over the next 18 months, just as the Federal Reserve thought it was taming price pressures. Core inflation, already running above the Fed’s 2% target, could accelerate toward 6% by mid-2026 if tariffs reach the levels Trump is suggesting.

But the real shock comes from GDP projections. Economic models predict the tariff escalation could slash U.S. GDP growth by 1.5-2% annually, effectively wiping out most economic expansion. That’s recession-level impact without typical business cycle triggers. Meanwhile, China faces a comparatively modest 0.8-1.2% GDP contraction, according to analysis by OECD economists.

The Economic Paradox: America’s Bigger Pain

The paradox deepens when you examine government revenue. While devastating the broader economy, tariffs would generate a Treasury windfall of $400-500 billion annually, equivalent to 18% of all household income tax payments. It’s a massive wealth transfer from consumers to government, funded by higher prices on everything from smartphones to steel.

Sector-by-Sector: Where the Pain Hits Hardest

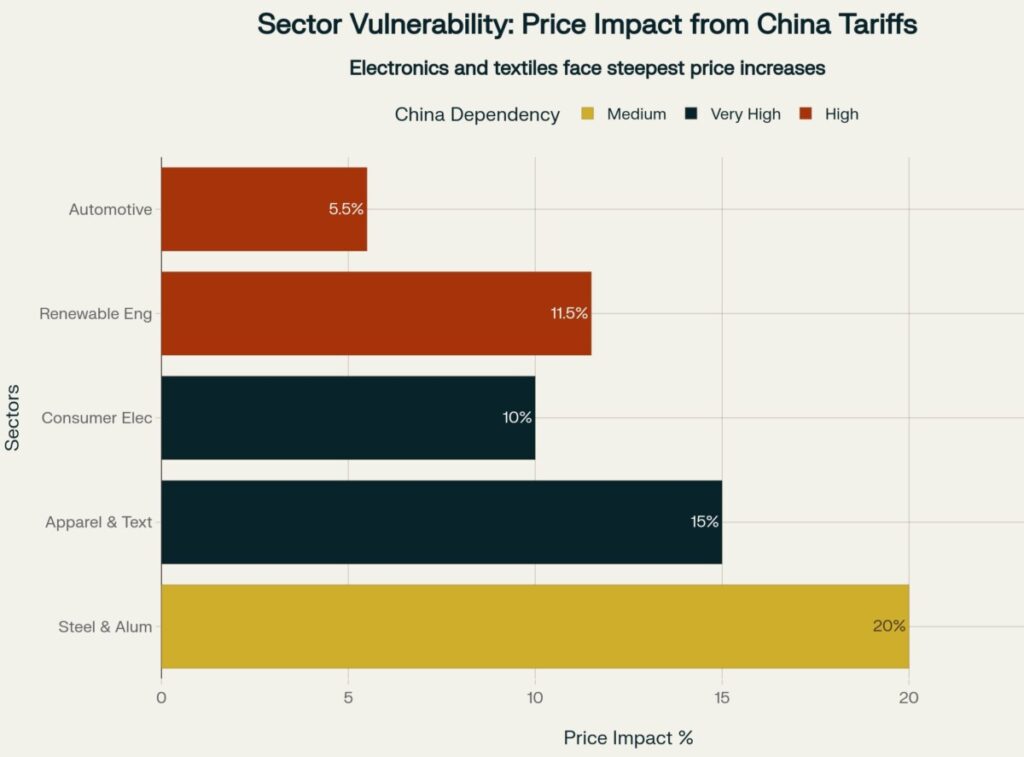

Consumer electronics face “extreme” vulnerability. Apple Inc. (NASDAQ:AAPL), despite ongoing production shifts to India and Vietnam, still depends heavily on Chinese manufacturing. Industry analysts estimate tariffs could add $200-300 to iPhone costs, testing consumer price elasticity at already-premium price points.

Automotive companies confront structural challenges that can’t be solved with alternative sourcing. Ford Motor Co. (NYSE:F) estimates tariffs could add $500-1,000 per vehicle in production costs. The industry’s complex supply chains (where a single car contains parts from dozens of countries) make quick substitution nearly impossible.

Steel and aluminum processors face the steepest consumer price increases, with costs expected to jump 15-25%. Construction and manufacturing sectors dependent on these inputs will face margin compression or must pass costs to end customers.

Apparel retailers like Target Corp. (NYSE:TGT) and Walmart Inc. (NYSE:WMT) face 10-20% price increases on clothing and consumer goods. However, these companies have demonstrated remarkable agility in sourcing diversification, potentially limiting long-term damage as they shift to Bangladesh, Vietnam, and other alternatives.

The Investment Playbook: Winners and Losers

Smart money is already repositioning. The main insight is that this is more than just about trade. It’s a fundamental restructuring of global supply chains that will create distinct winners and losers over the next 3-7 years.

Automation Gets Turbocharged

Companies providing supply chain technology and automation are seeing accelerated adoption as businesses scramble to reduce China dependencies. Honeywell International Inc. (NASDAQ:HON) and Rockwell Automation Inc. (NYSE:ROK) are building order backlogs as manufacturers invest in U.S.-based production systems. Manufacturing executives report focusing on supply chain resilience “front and center”, with automation spending priorities elevated.

Nearshoring’s Biggest Beneficiaries

Mexico emerges as the clearest winner from trade diversion. Companies with significant Mexican operations (like Caterpillar Inc. (NYSE: CAT) and General Electric Co. (NYSE:GE)) stand to benefit from USMCA advantages as production shifts from China. Trade data shows Mexico experiencing 15-20% increases in U.S.-bound manufacturing volumes since tariff threats intensified.

Domestic Manufacturing Renaissance

U.S.-based manufacturers with minimal China exposure become premium assets. Deere & Company (NYSE:DE) exemplifies this theme: American-made equipment with growing export potential as global buyers seek China alternatives. The challenge remains finding pure-play domestic producers after decades of supply chain globalization.

Fed Chairman Jerome Powell faces an impossible policy dilemma. Tariff-driven inflation demands higher interest rates, but the economic slowdown requires accommodation. Recent comments from Fed governors suggest growing concern about core inflation remaining above 2% through 2027, creating a prolonged stagflationary environment not seen since the 1970s.

This puts pressure on rate-sensitive sectors. Real estate investment trusts and utilities could face headwinds as the Fed prioritizes inflation control over growth support. Conversely, financial companies like JPMorgan Chase & Co. (NYSE:JPM) may benefit from sustained higher interest margins if rates stay elevated longer than markets currently anticipate.

Regional Power Shifts Accelerate

China’s response to tariff threats extends beyond tit-for-tat measures. Beijing is accelerating its pivot toward domestic consumption and alternative trade partnerships with ASEAN nations and the Global South. Alibaba Group Holding Ltd. (NYSE:BABA) and other Chinese tech giants are expanding aggressively in Southeast Asia and Latin America, creating new competitive dynamics that could persist for decades.

European companies face collateral damage from the escalating U.S.-China conflict. ASML Holding NV (NASDAQ:ASML) and other technology exporters could see 15-20% declines in combined U.S. and Chinese sales as retaliatory measures spread. The integrated global economy makes isolated trade wars nearly impossible, as pain spreads quickly across interconnected supply chains.

How to Position Your Portfolio

A balanced approach for the 12-18 month horizon allocates 40-50% to defensive positions: domestic-focused companies with minimal China exposure, inflation hedges including precious metals and commodities, and dollar-denominated assets benefiting from initial currency strength.

Opportunistic growth plays deserve 30-40% allocation: supply chain technology providers, automation companies, and alternative trade partner beneficiaries in Mexico and Southeast Asia. These themes offer 2-7 year investment horizons as structural changes play out.

The remaining 10-20% belongs in tactical positions around negotiation cycles, currency momentum plays, and regional trade diversion opportunities. These higher-risk allocations can capture volatility spikes around summit meetings and policy announcements.

Sector-by-sector vulnerability analysis revealing which industries will hit consumers hardest, with steel and aluminum facing 20% price increases despite only medium China dependency, while highly dependent sectors like electronics and textiles show significant but varied impacts.

In Summary

Trump’s tariff escalation threat represents more than trade policy. This is a fundamental restructuring of global economic relationships. While short-term costs appear substantial, the long-term implications may prove more significant than immediate GDP impacts suggest.

As Trump noted in his Truth Social post, there may be “no reason” to meet with Xi given China’s “hostile” rare-earth actions. This suggests the economic conflict will intensify before any diplomatic resolution emerges. Investors positioning for a quick deal may face disappointment. The winners will be those who adapt quickly: companies successfully navigating supply chain complexity, investors positioning for structural rather than cyclical changes, and nations capturing diverted trade flows. The old globalized system won’t simply snap back after political tensions subside. This is a regime change that will reshape capital allocation for years to come.

Featured Image Credit: Author

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.